To pay off the mortgage or not, the essential question all early retirees (except renters) must ask themselves. The folks that want to pay off their mortgage argue that no early retiree ever regretted NOT having a mortgage. I love the idea of not having a mortgage. And who wants to pay the extra hundreds of thousands on mortgage interest?

Those that do not want to pay off their mortgage in early retirement base their decision purely on the math. If you are paying 3 or 4% interest, you could be making 6-10% with that money invested. Not to mention, you have a way better shot at itemizing your taxes with that interest deduction (I know rules have changed, but it is still more likely with the interest than without).

Mr. FIF firmly believes we should not pay off the sub 3% mortgage. I want the lower monthly and annual expenses that come with not having a mortgage to pay for.

The compromise? I account for the mortgage separately from our FI Spending, with a different “bucket” of money. I don’t have a separate fund specifically dedicated to the mortgage, I just earmark part of the portfolio to pay the mortgage payment and don’t count the mortgage payment as part of my annual spending. This is probably more complex than it needs to be, but it makes me sleep better at night.

Ever since Mr. FIF took a stand on paying off the mortgage, I’ve been researching what approach to use to account for our mortgage in retirement. I’ll show you the math behind multiple approaches, run them through firecalc.com (online retirement calculator that I run most of my scenarios through), and then I’ll share which approach I’m using for my planning purposes.

We are about a year into a $463,518 mortgage. Holy cow you say, how does anyone pursuing FI have over a $400,000 mortgage? I thought we were supposed to be frugal? Well folks, there are six of us plus a dog and the one place in my budget that I haven’t been frugal is the house. We have never house hacked, nor do we ever plan to. I fully support house hacking if you are in a season of life that allows that. Housing is a huge expense, our biggest in fact. On the bright side, we got a damn good 2.875% interest rate on this mortgage. So our principal and interest payments are $1923/mo. Remember, real estate taxes and homeowner’s insurance aren’t going away even if the house is paid off, so we keep those expenses solidly in our annual expenses when calculating our FI number.

Other details we’ll need to compare our strategies are that we plan for a 3.5% safe withdrawal rate (SWR) and assume a portfolio return of 6.0%. For our $463,518 mortgage at 2.875%, we’ll pay a total of $692,316 in principal and interest over the life of the loan if we pay the mortgage as scheduled.

Strategy 1: Include in FI #

Now, the first and most conservative strategy is to act like you’ll be paying the principal and interest of a 30-year loan forever and add it to the expenses side of your FI calculation.

$1,923 x 12 = $23,076

$23,076/.035 = $659,314

The problems with this strategy are that the loan won’t be around forever AND my mortgage payment is inflation-protected. If I include the $23,076 in my annual expenses, the safe withdrawal rate assumes that those expenses will inflate.

Strategy 2: Payoff Set Aside

Another simple strategy, though not as conservative is to just add the balance of the mortgage to your portfolio. So the payoff set aside here is $463,518, or whatever the balance of the mortgage is at the time you FIRE.

This money could be used to pay off our loan anytime, but this strategy doesn’t account for the interest we are still paying every month when we don’t pay it off. We just assume that the payoff set aside portfolio will make at least 2.875% (which is pretty safe considering our safe withdrawal rate is higher than that). So is this amount still too conservative for our FI planning?

Strategy 3: Drawdown

The last strategy is to set aside a portfolio value large enough that you can draw down the portfolio to zero over the life of the mortgage. I came across this reddit/financial independence page, How to Calculate Your FIRE Number When You Have a Mortgage (with Spreadsheet!).

The drawdown strategy is planning an investment amount that you can draw down to zero over the life of the mortgage.

To get a value for this strategy, use a “present value” formula in your favorite spreadsheet. This one works in either Excel or Sheets: PV(rate, number of periods, monthly payment, payment made at beginning or end of period).

Just remember to make sure your periods are consistent. Since we will use monthly payments, the rate and number of periods should also be by month. Our interest rate is an annual rate, so we divide by 12 to get the monthly rate. Staying consistent, we multiply our 30-year mortgage by 12 for a 360 period.

PV(2.875%/12, 360, -$1923, 0) = $320,757

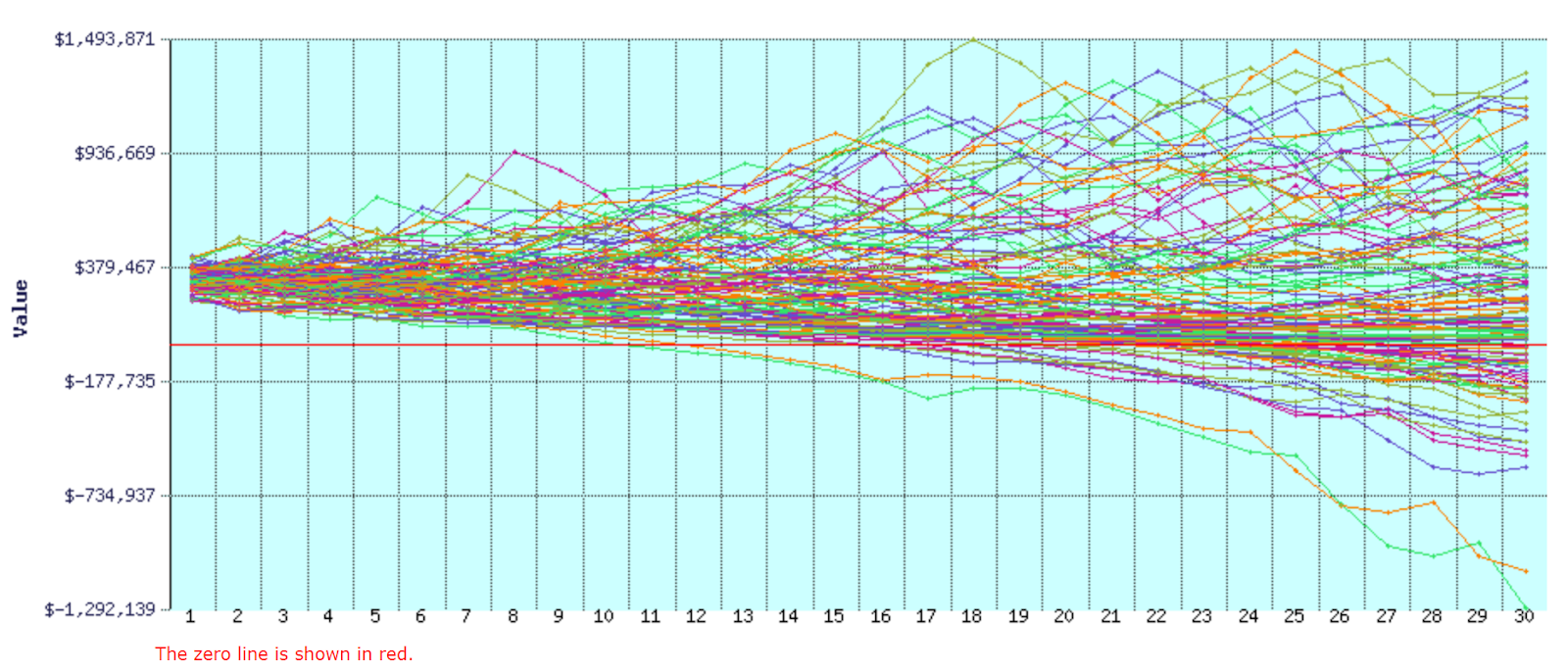

That is less than half of the portfolio needed for strategy 1! When I first dug into the reddit post, I was ecstatic. It took years off of my FI projections. I wanted to believe it so badly. As I sat with it and turned it over in my head, it began to feel too good to be true. Enter FIRECalc, one of my favorite online retirement calculators.

I used the $320,757 as my portfolio value with no spending. Any spending entered on the first tab will be adjusted for inflation based on what options you choose on the “Spending Models” tab. Instead, I enter the annual mortgage payments in the “Other Income/Spending” tab so I can remove the inflation adjustment to our spending. The Off Chart Spending is the annual expense of the mortgage, and the Pension Income is used to reduce the off chart spending when the mortgage is paid off. I also adjusted the “Your Portfolio” tab to match my stock weight (85%) and fees (0.13%).

FIRECalc looked at the 120 possible 30-year periods in the available data, starting with a portfolio of $320,757 and found a success rate of 67.8%! I don’t know about you, but I can’t sleep at night with a 67.8% chance that I’ll be able to afford to continue paying my mortgage. I don’t know how FIRECalc does it, but the output graph looks exactly like how I feel with a 67.8% success rate.

Now that we’ve explored all of these strategies, thanks to FIRECalc, we have come around to the strategy I currently use to account for my mortgage in my FIRE calculations.

Strategy 4: Estimate Based on Historical Returns

Close to a 33% failure rate makes me pretty uncomfortable. I decided that maybe my 6% market return assumption (that got me to my original $320,757 drawdown amount) may have been too optimistic. So I ran the following numbers through the calculator to get a drawdown estimate I was comfortable with.

| Assumed Market Return | Starting Portfolio Value | FIRECalc Success Rate |

| 6% | $320,757 | 67.8% |

| 5% | $358,238 | 85.1% |

| 4% | $402,815 | 96.7% |

| N/A | $400,000 | 95.9% |

I’m shooting for a 95% success rate, but I also like big round numbers. So when I saw $402,815 overshot 95%, I rounded down to $400,000 and put it in FIRECalc to make sure I liked what I saw.

$400,000 is the portfolio value I set aside to cover our mortgage for early retirement.

What do you think, is my number too conservative, too risky or just right?